Developing captives allows the market to elevate Hong Kong’s value chain in the insurance business. Nurturing talent, refining regulatory regimes and bolstering demand will help the city’s nascent industry ecosystem grow. Oswald Chan reports.

Editor’s note: Hong Kong is polishing up its world financial center standing by allowing companies to manage all sources of business and financial risks. The second article of our series examines how the captive insurance segment is upgrading the city’s value chain in the insurance industry.

Global conglomerates face diverse and complex business risks like natural disasters, environmental liabilities, cybersecurity threats, supply-chain disruptions, property damage and general liabilities in various markets.

Traditional commercial insurance solutions cannot bring economies of scale, as they entail high premiums and limited coverage that will stretch corporate cash flows.

The panacea is to get a captive insurance company going — a wholly-owned subsidiary of a conglomerate that provides risk mitigation for its parent company or related entities.

READ MORE: AIA's new business value climbs in Q1 on strong mainland, HKSAR demand

By eliminating the third-party insurer profit margins, setting up a captive insurer would mean potential cost savings, significant tax benefits, underwriting profits, improved cash flows, as well as greater control over coverage and claims. Coverage gaps could also be addressed when commercial insurers could not or would not cover certain risks.

But, there are drawbacks in using captive insurance, such as potentially high overhead costs, compliance issues and the risk of being underinsured.

According to Captives.Insure, there were nearly 8,000 captive insurance companies worldwide in 2024, with the state of Vermont in the United States, Bermuda, the Cayman Islands and Singapore being major captive insurance hubs.

Bermuda is the leading captive insurance center with over 600 active captives in 2024 and specialized managers and lawyers, leveraging its mature ecosystem and proximity to the US market. Singapore leads the Asia-Pacific region with about 90 captives, serving as the primary hub for Southeast Asian and Australian companies.

The Hong Kong Special Administrative Region government first prioritized nurturing the captive insurance industry in its 2024 Policy Address, following the promulgation of the 14th Five-Year Plan (2021-25) by the central government that emphasizes Hong Kong as an international risk management center.

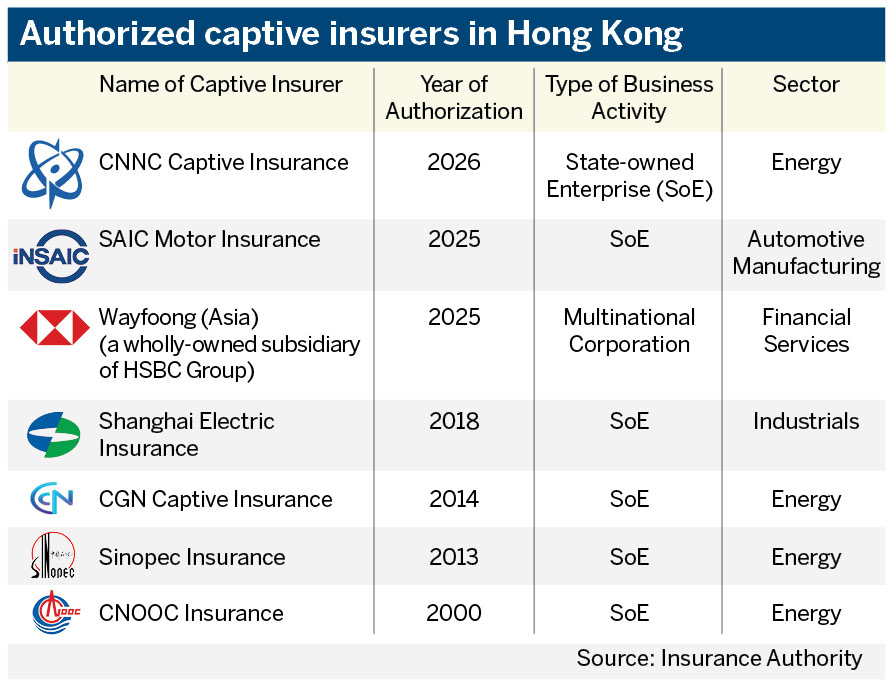

The city is now home to seven captives that were authorized between 2000 and 2026. Their parent companies are mainland state-owned enterprises and a multinational company with business sectors spanning energy, industrials, automotive manufacturing and financial services. HSBC Group’s Wayfoong (Asia) marked a milestone as the first multinational enterprise to secure a captive license in Hong Kong.

Challenges to tackle

According to the Insurance Authority’s 2025 provisional statistics, the gross premium generated from the SAR’s captive business hit HK$2.13 billion ($272 million) last year. Hong Kong’s position in the captive insurance sector, however, does not match its status as a world insurance hub. Hence, improving the supply-and-demand dynamics is needed to cement the city as a captive insurance hub in the Asia-Pacific region.

Hong Kong does not have a sizeable specialized talent pool in captive to support the ecosystem, as such expertise is largely concentrated in a few brokerage firms and several captives themselves. Captive insurance management demands actuarial modeling, underwriting capability and strong governance, as well as regulatory and financial reporting.

“Hong Kong’s captive insurance business still lacks scale and volume. Most industry players are not deeply anchored in a local captive cluster, and dedicated captive management expertise has yet to emerge rather than being deep and broad,” says Chng Tze-ping, Greater China financial services Hong Kong market leader and Hong Kong risk consulting leader at EY.

Deloitte China Consulting Director Kelly Xu Qianqian suggests that Hong Kong introduce accreditation programs to develop expertise in captive management, cross-border reinsurance, legal and accounting services. Financial regulators must encourage banks and asset managers to create tailored products for local captives, such as specialized treasury and investment services, she says.

“Hong Kong should consider relevant professional certification programs and strategically attract talents from other captive insurance hubs through its Top Talent Pass Scheme and the Quality Migrant Admission Scheme,” says Joe Zou Hong, a professor at HKU Business School.

Besides the talent gap, there is also an awareness problem. Zou says Chinese mainland private corporations and medium-sized state-owned enterprises still do not fully understand captive insurance. “The HKSAR could establish a special task force to reach out to large non-SOEs and sizable SOEs with educational initiatives to help them recognize and embrace captive insurance as an enterprise risk management tool,” he says.

Such educational work is being done with the Insurance Authority hosting a captive forum in Beijing in March this year, drawing nearly 100 mainland and Hong Kong participants from enterprises, captive insurers, reinsurers and professional service providers.

Hong Kong’s regulatory regime for captives is tailored exclusively for wholly-owned and single-parent captives which is often too expensive. And the scope of insurable risks is largely confined to the risks of their parent companies and related group entities.

“By allowing firms to rent a cell in an existing captive instead of building one from scratch, the protected cell company (PCC) structure would make Hong Kong much more attractive to medium-sized firms and Belt and Road subcontractors with smaller risk portfolios. At present, Singapore does not permit a protected cell company structure and, hence, any jurisdiction that is the first to allow it might be a game changer for competition,” says Zou.

“Subject to clear safeguards, if we allow captives in Hong Kong to cover risks of strategic joint ventures or selected customer-related financing exposures, it could help many mainland conglomerates involved in BRI projects,” he says, adding that such legislative changes could prevent mainland conglomerates from reverting to traditional commercial insurance that may be unavailable or too expensive for project-specific risks.

Clement Lau Chung-kin — policy and legislation executive director with the Insurance Authority — says it is working on a study on the feasibility of introducing PCC, as well as adopting a more flexible approach to assess the scope of risks that can be written by a captive, with a view to allowing more tailored solutions for companies to address various emerging risks, and enhancing the overall attractiveness of Hong Kong as a captive domicile.

The SAR already has a dedicated regulatory regime in place for captives operating locally with simplified capital requirements and profits tax concessions. These companies already enjoy a 50-percent profit tax rate concession (of 8.25 percent), covering insurance business profits arising from offshore and onshore risks. The capital base for such captives must not be less than HK$2 million — significantly lower than the at least HK$20-million requirement for general business insurers.

The regulatory regime also provides for the expedited authorization process of captive insurers, streamlined reporting requirements and flexibility to conduct full or partial key function outsourcing. Captives in the SAR are exempted from appointing a certifying actuary, and they are also exempted from the requirement to maintain assets in the city to match local liabilities.

Zou says raising the 50-percent profit tax concession for captive insurers is still inadequate for cementing the industry ecosystem. “The lack of sufficient independent captive insurance managers is a key weakness. Offering tax credits to independent captive managers and consultants would attract them to the city and make them lower their fees,” he adds.

Demand and opportunities

With the recent regulatory revamp, Chng expects the next wave of regulatory enhancement to shift toward deepening the captive ecosystem. “One area for improvement is to ensure that the regime remains flexible enough to accommodate emerging risks like cyber threats, environmental, social and governance (ESG) liabilities, and supply-chain disruptions where commercial insurance capacity or pricing may be constrained,” he says.

Strengthening demand for captive insurance services is also important in lifting the industry ecosystem. The demand driver comes from company redomiciliation, along with infrastructure development in Belt and Road countries, and the Guangdong-Hong Kong-Macao Greater Bay Area.

Financial Services Development Council Executive Director Rocky Tung Yat-ngok tells China Daily: “If Hong Kong wants to promote the captive insurance business, it should do more to get more companies to set up their regional headquarters or treasury centers in the city.”

He expects mainland and global corporations with the bulk of their revenues generated in Asia or the Greater China region to choose Hong Kong for redomiciliation and establishing their regional headquarters.

By May, a year since the company redomiciliation regime was introduced, Hong Kong had attracted 36 companies with 21 applications still to be processed, according to Financial Services and the Treasury Bureau. The regime allows non-Hong Kong-incorporated companies that fulfill the requirements on company background, integrity, member and creditor protection, as well as solvency, to apply to redomicile to the SAR.

Hong Kong’s strategic proximity to the mainland, close integration with the Greater Bay Area and its involvement in the Belt and Road Initiative empowers captives in Hong Kong to serve the mainland’s SOEs and multinational conglomerates, unlike Bermuda’s global focus or Singapore’s regional logistics emphasis.

“The establishment of captives becomes particularly relevant when enterprises venture abroad or participate in large-scale projects, such as those under the Belt and Road Initiative, in which captives can help enhance their resilience in response in complex risks,” says Lau.

The Insurance Authority will target large enterprises with significant and complex risk-management needs, including mainland SOEs and private companies, as well as multinational conglomerates with a substantial business presence in Asia, to establish captives in Hong Kong.

In Zou’s view, the Belt and Road Initiative is a powerful engine for mainland conglomerates to establish captives in Hong Kong. “By using a captive in Hong Kong, a mainland conglomerate can navigate complex overseas risks associated with large-scale projects, retain direct control over risk protection, and ensure its projects are covered even when the commercial market is tight,” he says.

He says Hong Kong’s capital market can offer competitive rates for conglomerates to gain access to international capital from global reinsurance markets.

ALSO READ: Disaster bonds fortify hub

Chng expects enterprises in the electric-vehicle, robotics and artificial intelligence sectors to opt for captive insurance as they have difficulty in obtaining comprehensive commercial insurance due to the lack of data for underwriting and pricing.

Chng says promoting the captive insurance business in Hong Kong will upgrade the city’s value chain in the insurance industry from a traditional insurance market to a comprehensive risk management and risk financing hub.

Joanna Wong Chung-yen, national insurance leader at Deloitte China, says elevating the captive insurance business will extend the city’s insurance market from personal protection to corporate risk management.

“Captives encourage the expansion of tailored financial services, incentivizing banks and asset managers to innovate dedicated treasury, custody, and institutional investment solutions,” she says. “And, Hong Kong’s regulatory excellence in captive supervision helps reinsurers and insurance-linked securities players to establish an integrated risk financing center, supporting complex insurance activities like cyber, ESG, and catastrophe risk transfer.”

“A strong captive insurance market would also enhance Hong Kong’s significance in capital and risk management while acting as a magnet for professional services,” says Zou.

Contact the writer at oswald@chinadailyhk.com