China’s new energy vehicles business has come a long way since Shenzhen laid the foundation 17 years ago by leading a national NEV initiative. As Stacy Shi reports, the momentum generated by the Guangdong-Hong Kong-Macao Greater Bay Area has pushed the industry to great heights.

About half an hour’s drive from Shenzhen’s city center, a vast industrial landscape looms over the northeastern district of Pingshan — with block after block of factories, research and development facilities, as well as warehouses. It’s the heart of Shenzhen’s ambition to build a “world-class new-generation automotive city”.

Pingshan aspires to be Shenzhen’s “new growth pole”, a “model for scientific growth” and a vital gateway of China’s southern technology pivot in Guangdong province — the home of BYD, the nation’s largest maker of new energy vehicles.

But the story of the Guangdong-Hong Kong-Macao Greater Bay Area’s electric-vehicle industry extends far beyond one enterprise.

READ MORE: Smart driving reshapes trend at Auto Guangzhou

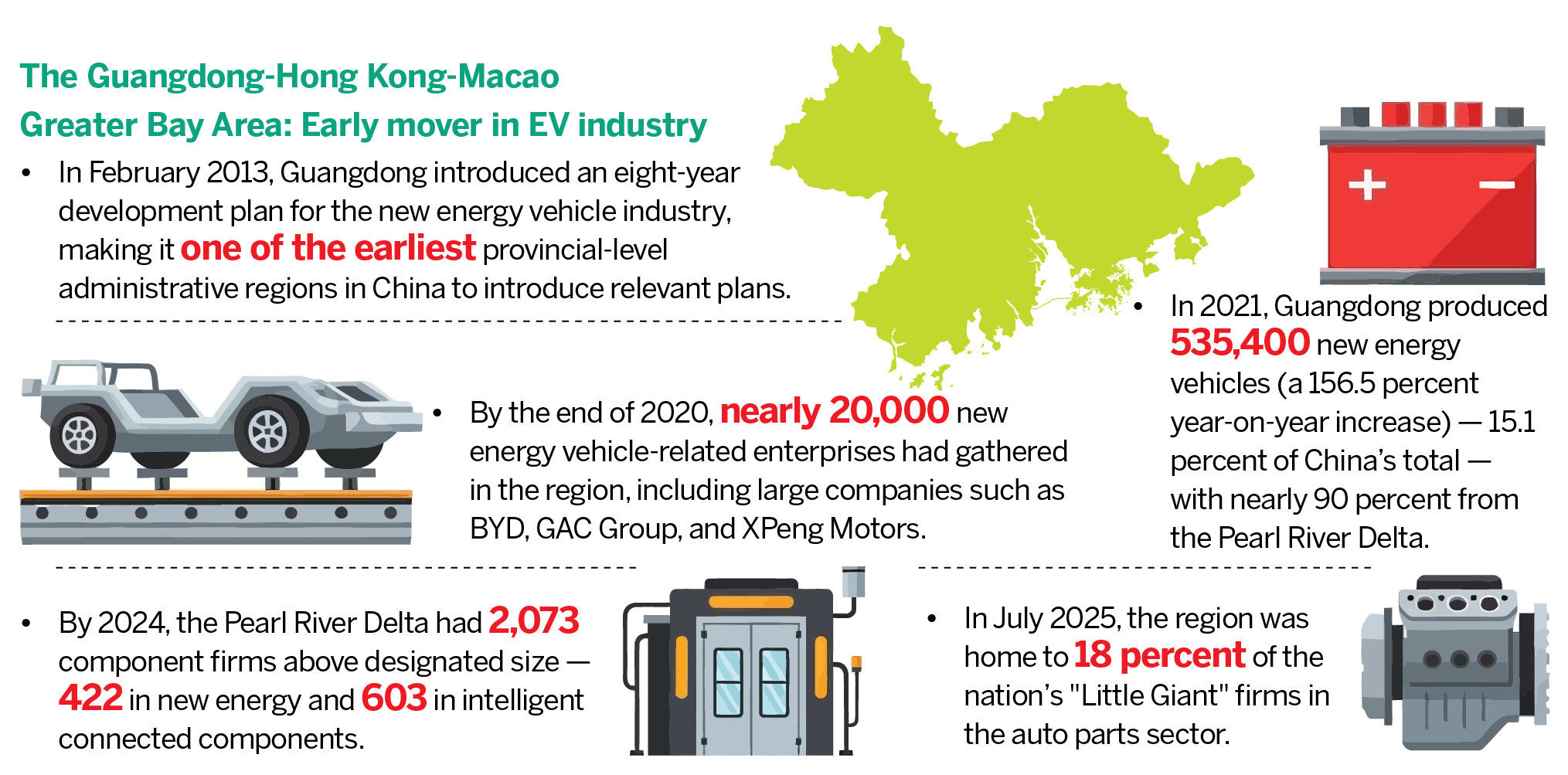

The statistics are staggering. In 2024, Guangdong produced over 3.61 million NEVs, accounting for a quarter of the country’s total. As of that year, the Pearl River Delta had hosted more than 2,000 automotive component firms above designated size — 422 in new energy components and 603 in intelligent connected systems, with 18 percent of the nation’s innovative companies, dubbed the “Little Giants”, specializing in the auto-parts sector, having set up shop in the region as of July 2025.

The EV story isn’t merely about scale. It’s also about density, speed and an ecosystem that insiders call the “two-hour supply circle” — a supply chain centered on Shenzhen and the provincial capital, Guangzhou, that spans the entire province and neighboring Guangxi Zhuang autonomous region.

The NEV ecosystem didn’t emerge by chance. Its foundation was laid more than 17 years ago. Chan Ching-chuen, called the “father of Asian electric vehicles”, reminisces about how Shenzhen led the pack with a “10-city, 1,000-vehicle” program — a national initiative launched in January 2009 that deployed 1,000 NEVs in each participating city with public and government fleets, backed by generous subsidies. Shenzhen was among the first 13 cities chosen for the exercise.

“Shenzhen was very smart. It converted taxis and buses into electric vehicles, giving EV-makers, such as BYD, real orders. Once people saw EVs running on the streets, they believed it could work,” Chan says.

To date, the region has hosted industry-chain leaders, not just BYD, Guangzhou Automobile Group or XPeng Motors, but also countless suppliers. Among them, a dense network of suppliers has taken shape.

BTR New Material Group (BTR) — a leading battery-materials supplier based in Shenzhen — embodies such an advantage. “A complete industrial chain means our manufacturing business has a competitive edge,” says Xu, a technical representative of the company that supplies anode materials for battery producers such as CATL, BYD, EVE, Panasonic, LGES, SK On, and Samsung SDI. “And, because everything connects within the region, our advantages are obvious.”

Xinmei Electron — a Dongguan-based supplier of specialized adhesive tapes used for lithium batteries — traces the region’s roots even further. “The battery sector started in Dongguan, with Amperex Technology. The entire Greater Bay Area has complete supporting facilities for batteries,” says Xinmei’s sales director, Geng Chaowei. “Many battery manufacturers elsewhere in China still source their suppliers from here.”

Currently, tabless technology and large volume give batteries distinct advantages with significantly lower internal resistance, higher energy density, improved thermal management, and an extended life cycle with improved safety. These features suit demanding applications, including EVs, eVTOL (electric vertical takeoff and landing) aircraft, and high-rate energy storage, explains Chu Lingling, general sales manager of Ningbo-based Yunsa Power in Zhejiang province, which produces these large cylindrical full-tab batteries, but is still drawn to the region’s gravitational pull with a research-and-development center in Huizhou.

This clustering effect extends beyond the Greater Bay Area’s core cities. While Shenzhen and Guangzhou anchor the ecosystem with their headquarters, surrounding cities have carved out special roles for themselves. Dongguan, with its manufacturing DNA, houses countless component makers, while Foshan and Zhaoqing have attracted battery and materials investments.

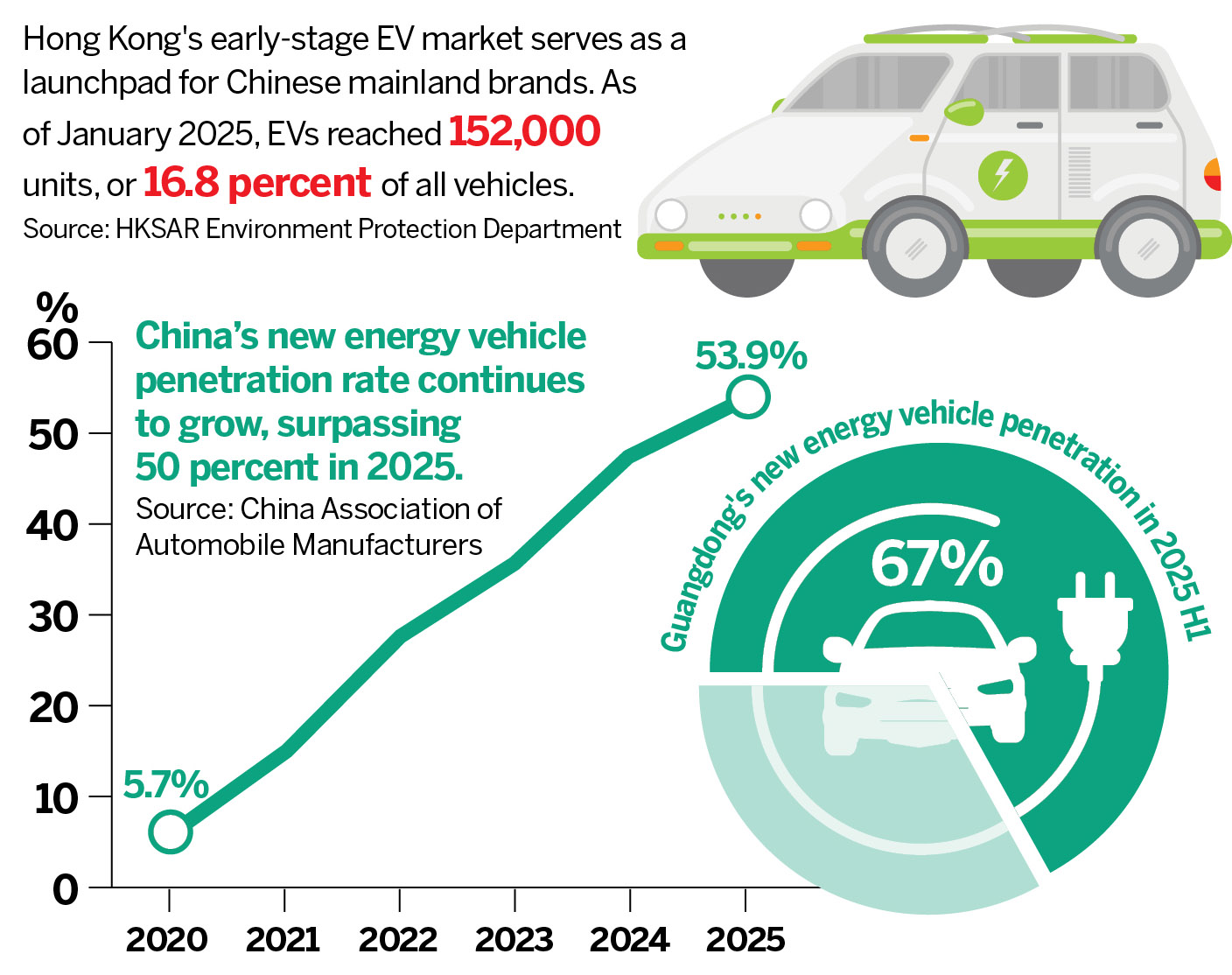

The momentum generated by Greater Bay Area has propelled China’s new energy vehicle industry to remarkable heights. Nationwide, last year’s automotive production and sales had surpassed 34.4 million units, with nearly 16.5 million NEVs sold — a 28.2-percent year-on-year increase, with a domestic penetration rate having exceeded 50 percent for the first time.

From local to global reach

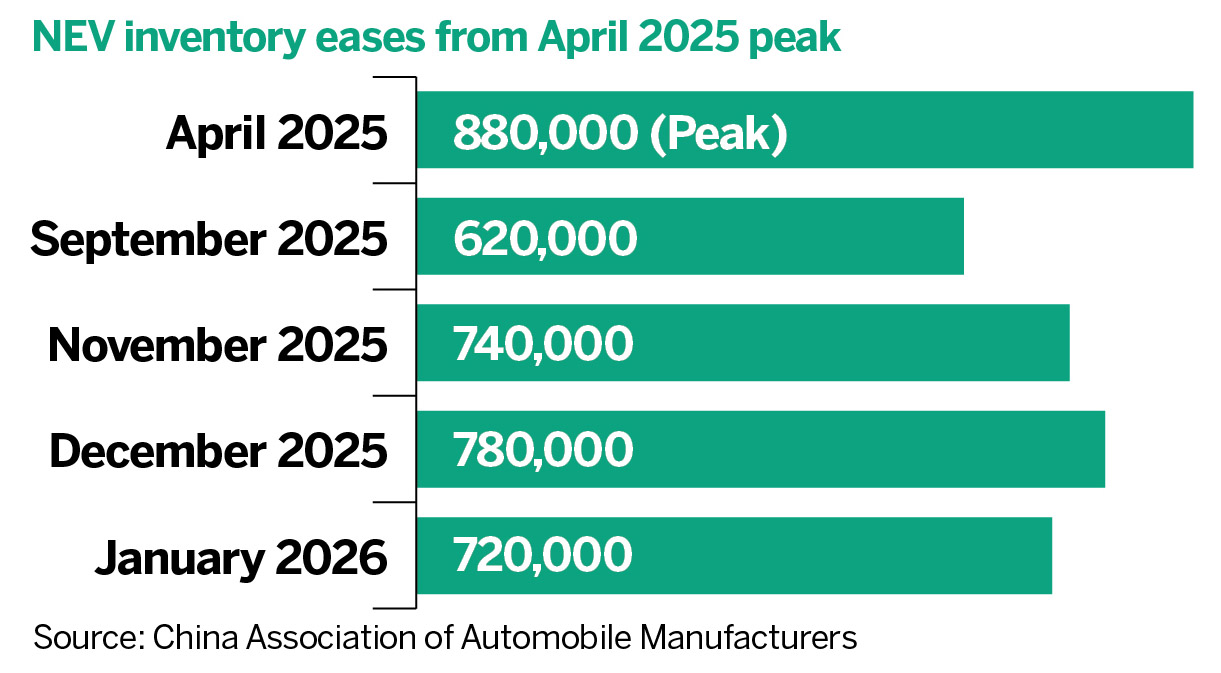

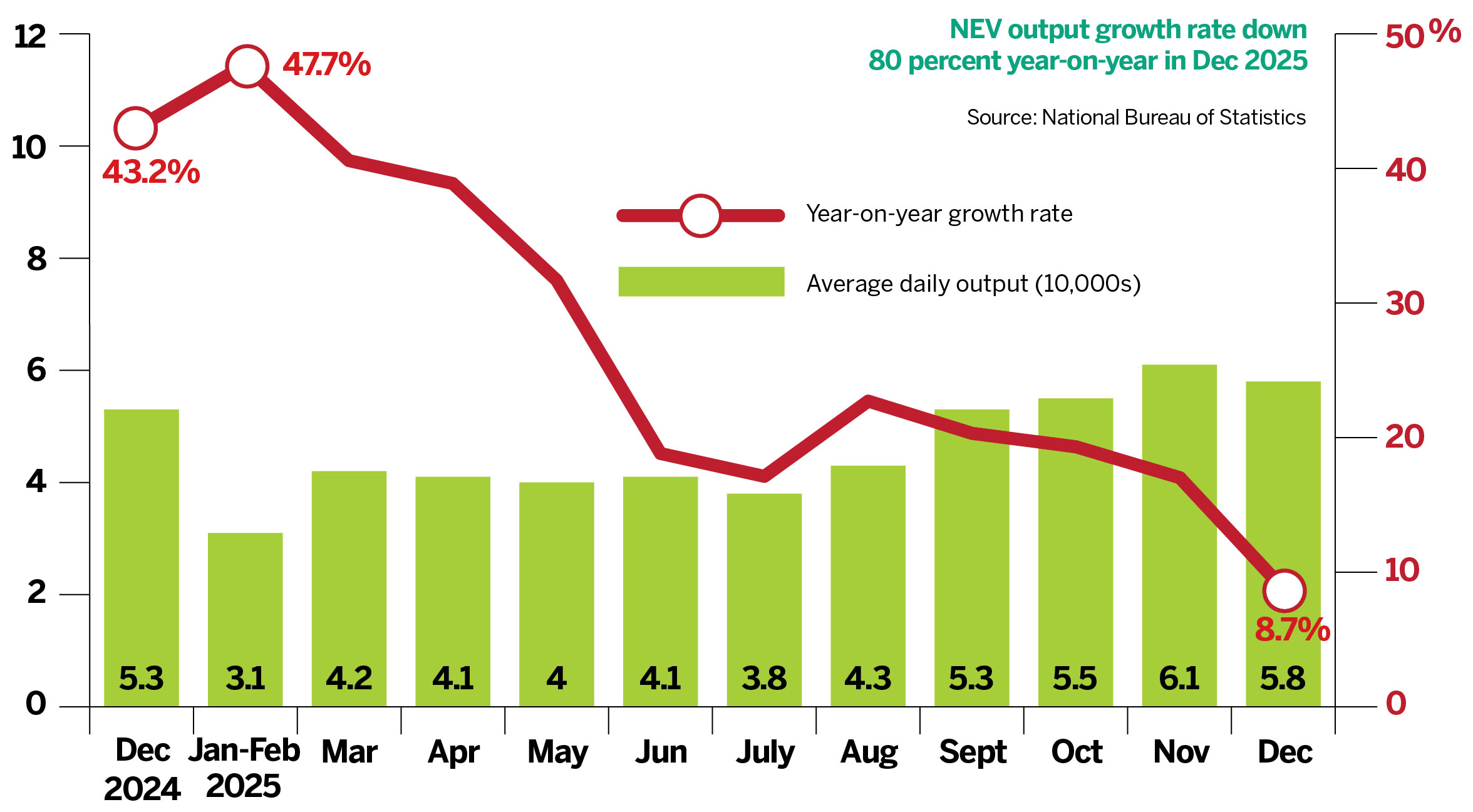

Yet, as the industry matures, scale alone no longer tells the full story. Behind those impressive numbers, signs of strain have emerged. By January this year, national passenger vehicle inventory stood at 3.57 million units — 580,000 more than that of the same month in 2025, representing roughly 70 days of supply and significantly higher than the 48-day level a year earlier — according to Cui Dongshu, secretary-general of the China Passenger Car Association. For NEVs, specifically, inventory climbed to 720,000 units, reflecting market demand having fallen short of expectations.

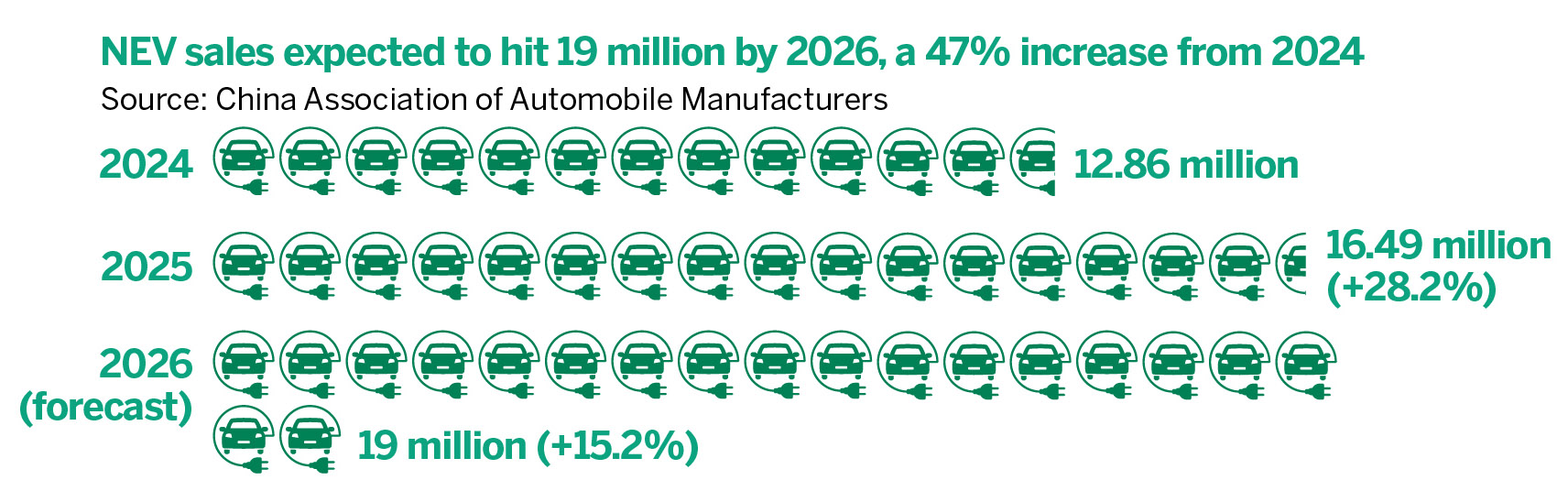

Growth is also decelerating. After years of exponential expansion, the China Association of Automobile Manufacturers expects sales of 19 million new-energy units for 2026 — a modest 15.2 percent year-on-year rise compared with 28.2 percent last year.

Meanwhile, the domestic penetration rate has topped 50 percent. The industry has entered what analysts describe as a transition from “incremental growth” to “stock competition”. And, with this transition comes a phenomenon Chan doesn’t shy away from. “We’ve a problem of vicious competition.” As growth slows, pressure cascades downstream. “Some vehicle manufacturers have put pressure on component suppliers, making it hard for some component companies to survive.”

The result, he says, may ultimately prove necessary. “Eliminating companies without real substance is required. There are hundreds of EV manufacturers in China.” The solution, he stresses, is competition based on core technology, rather than relationships or subsidies. “Healthy competition relies on your technology, your brand, your internal strength.”

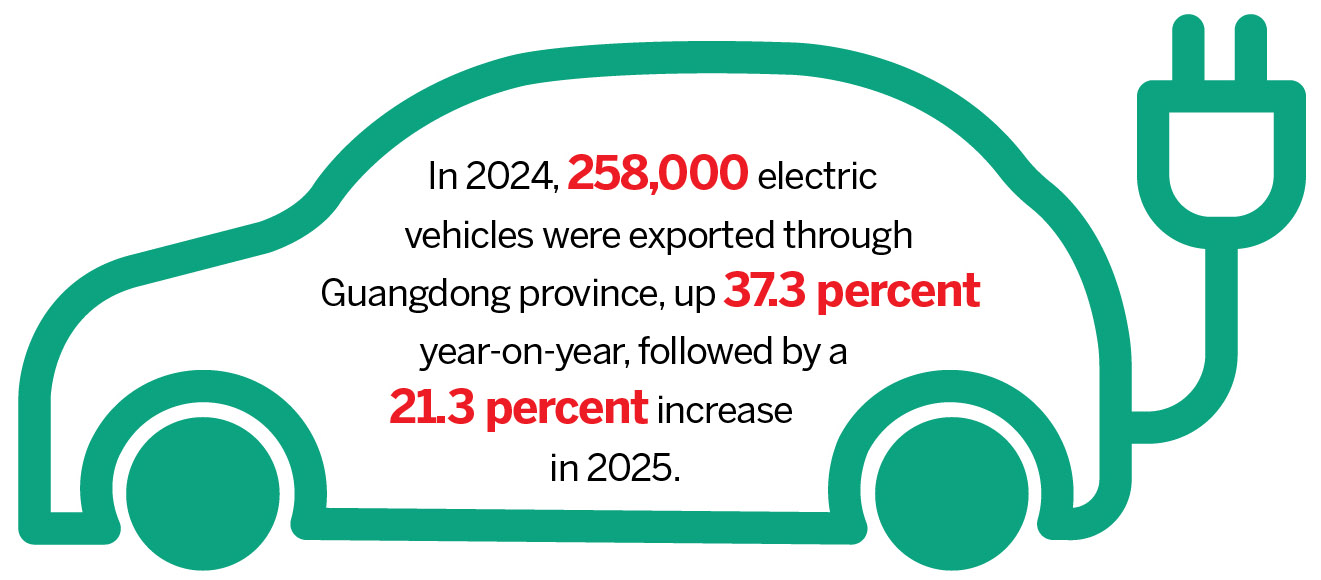

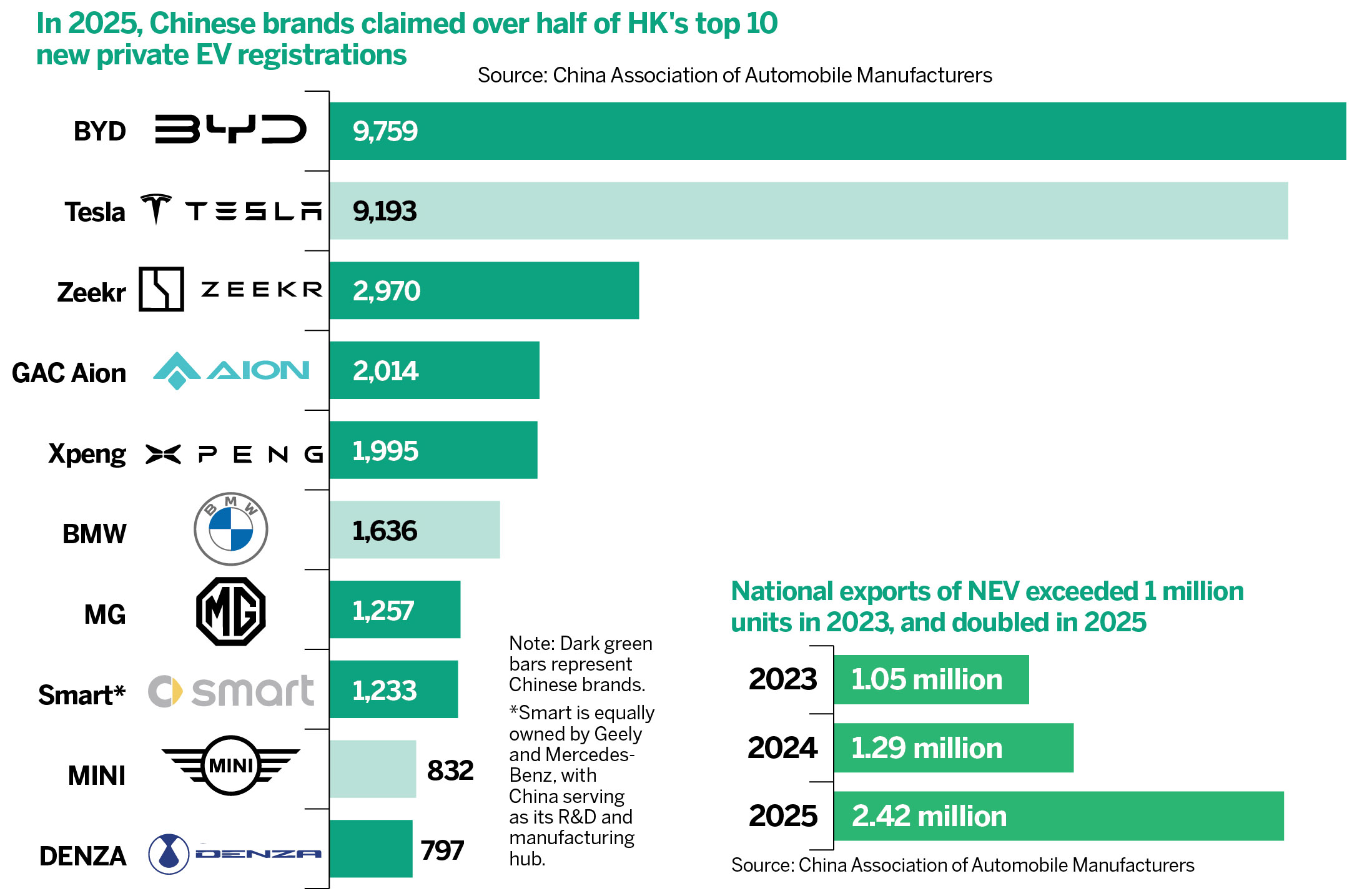

With domestic consumption exceeding 50 percent, overseas markets have become the next frontier. National passenger EV exports had surged from 1.05 million units in 2023 to 2.42 million last year, while Guangdong’s exports grew by 21.3 percent in 2025 alone.

But for exports, Chan cautions, it’s not simply shipping automobiles. He offers two principles for successful internationalization. “First, Chinese technology with local flavor” — success abroad calls for a deep understanding of local policies, regulations and culture. “If you’re going to Indonesia, you must understand Islamic culture. You must understand local geography and climate conditions,” Chan says.

The second principle is “Chinese genes with a local carrier”. Technology alone isn’t sufficient. It must be carried by local partners. “You’ve to collaborate locally. Your technology needs a local partner to truly take root,” Chan says. This is where Hong Kong enters the picture, not as a manufacturing hub, but as a strategic enabler for the companies built within the two-hour supply circle.

The special administrative region’s EV market remains modest in absolute terms, with some 149,000 vehicles as of December, representing 16.3 percent of total vehicles. But its strategic significance far exceeds the numbers.

Du Yonghai, chief innovation officer of the Hong Kong Productivity Council (HKPC), puts the market’s growth in perspective: “The Chinese mainland has had over a decade of accumulation. Hong Kong reached this percentage in just a few years. That’s not easy. And, now, over 70 percent of new vehicle registrations are EVs. Consumer acceptance has formed. The passenger car market will continue growing naturally. That trend is certain.”

Last year, Chinese vehicle brands claimed seven of the top 10 spots in Hong Kong’s new private EV registrations. BYD led with 9,759 units, with Zeekr, GAC Aion and XPeng also among top five. For BYD Hong Kong, this represents more than local sales.

“The most important breakthrough isn’t the sales figures alone,” says Raymond Cheung, chief operating officer of BYD (HK) Co Ltd. “It’s winning consumer trust and breaking preconceptions about Chinese brands. In a mature market gathering global top brands, BYD has proved that Chinese brands can reach world-class levels with technology and quality.”

This trust translates directly into export credibility. The auto giant’s ATTO 3 model became a global phenomenon, and Hong Kong played a pivotal role. “We systematically summarized the Hong Kong market experience — marketing strategies, user feedback, service systems — and applied it directly to other right-hand drive markets like Thailand, Australia, the United Kingdom and Japan. Hong Kong’s success has laid the foundation for ATTO 3 to become a global hit,” says Cheung.

He calls Hong Kong consumers “sophisticated and mature” who pursue the cost-performance ratio — price-sensitive, but focused on value, expect advanced technology, rich features, and reliable quality at reasonable prices.

Bridging gaps

The HKPC, through its Centre of Advanced Power and Autonomous Systems (APAS), offers a more granular view of the city’s value proposition. Established 20 years ago, the center has evolved from serving local users to not only connecting mainland innovation and global markets, but also providing value-adding services.

“Hong Kong boasts excellent fundamental research,” says Du. “But we have limitations — in industry scale, application scenarios. Chinese mainland complements these gaps.”

This synergy manifests in concrete projects. Du refers to the low-altitude economy applications as an example. APAS develops battery technologies in Hong Kong, but conducts flight tests with mainland partners, feeding performance insights back for refinement. Conversely, mainland companies seeking right-hand-drive markets use Hong Kong as a test bed. “Hong Kong’s driving behavior resembles that of Southeast Asia, following closely, but disciplined. It’s an ideal test field for right-hand-drive adaptation,” Du says.

As global trade barriers multiply, such as the European Union’s introduction of the Carbon Border Adjustment Mechanism to prevent “carbon leakage” by imposing a carbon price on carbon-intensive imports to match costs with EU-produced goods, compliance becomes a competitive differentiator. Hong Kong’s professional services ecosystem offers solutions.

“Many companies haven’t realized how these regulations will affect them,” Du says. “Even if you build factories overseas, you still need to understand local rules.” The HKPC’s “The Cradle — Go Global Service Centre”, offering one-stop support for technology enterprises and small-and-medium enterprises to expand internationally and set up last year, has received over 450 cases, helping companies to navigate international standards, legal compliance and localization.

The HKPC is also actively promoting the SAR’s local EV development, particularly in segments where the city can carve out a competitive niche. “The next frontier for electrification is commercial vehicles,” Du says. “Hong Kong has about 160,000 commercial vehicles — buses and trucks. Their electrification rate is still low.”

The council is developing tailored solutions — pantograph charging for electric minibuses by allowing minibuses to rapidly recharge to 80 percent capacity within the five-to-eight-minute rest period at terminal stations; exploring multi-module systems combining batteries with hydrogen or green methanol for commercial vehicles; and new materials to reduce the weight of vehicles, especially heavy trucks; and improving the electric range without compromising safety.

When it comes to autonomous driving, Du pushed back against perceptions that Hong Kong is lagging behind. “That’s a misperception,” he argues, adding that the APAS was among Hong Kong’s first autonomous driving R&D institutions, and conducted the city’s first public-road trial — a 5G-connected driverless minibus in a residential estate.

However, public roads pose different challenges. “Take the width of lanes, for instance. On the mainland, motor lanes are typically 3.5 meters wide. In Hong Kong, they’re just 3 meters. Even half a meter less alters safety margins and the way autonomous algorithms must function,” says Du. “In addition, average urban speeds tell a similar story — large mainland cities like Beijing and Shanghai average under 20 kilometers per hour, while Hong Kong averages over 30 km/h, sometimes reaching 50 to 60 km/h.”

Hong Kong’s terrain adds complexity, with its steep slopes, tight curves, and roundabouts without traffic lights. “These all require autonomous adjustment. Mainland autonomous driving may look advanced, but every application scenario requires recalibration. You cannot simply transplant technology to a different city and expect it to work.”

As the industry accelerates into a new phase, Chan’s vision captures the profound transformation underway. “The electric vehicle revolution is first about electrification, but it’s now moving toward intelligence and connectivity. I use two metaphors — the heart, the power generator of the automobile has changed, and so has its brain.”

While internal combustion engines once dominated, electric motors now take over. But the deeper shift lies in energy itself. “Electricity is bidirectional. The grid can charge EVs, but EV batteries can also feed energy back when needed. This opens infinite possibilities for vehicle-grid interaction. Previously, gasoline and diesel flowed only one way. Now, energy flows both ways.”

The brain has transformed even more dramatically. “With artificial intelligence, EVs have become smarter.”

Chan says that these twin transformations expand the entire industrial ecosystem and redefine what an automobile truly is. “It is no longer just a means of transport. It becomes humanity’s third space — first your home, second your office, and third your auto. With autonomous driving, you can do whatever you like inside… Mobility is freedom. Mobility is happiness.”

Toward broader market

The path forward, Chan says, lies in two directions — integration and internationalization. Integration means deepening the technological ecosystem — vehicle-grid interaction, satellite connectivity, and the fusion of human, vehicle and road. Internationalization means moving from exporter to global standard-bearer. “We must raise our international status, our voice and our standards.”

Recent developments underscore this direction. BYD unveiled its second-generation blade-battery and flash-charging technology on March 5, setting a new global record for the fastest charging speed among mass-produced vehicles — 10 to 70 percent in five minutes, and 10 to 97 percent in nine minutes at normal temperatures. In -30 C, charging from 20 to 97 percent takes only three minutes longer.

The message is unmistakable. The race is no longer about who can produce more, but who can innovate faster, charge quicker, and push technological boundaries further.

ALSO READ: BYD leverages tech innovation to navigate global trade challenges

Several days later, at the Battery Show Asia 2026 in Hong Kong, BTR took the stage to introduce two ultrafast charging graphite anode products — T-Max and T-Pro.

Through Hong Kong’s platform, industry players from the Chinese mainland, Japan, South Korea, Southeast Asia, India, Europe and the United States are seeking breakthroughs and overseas partners by looking beyond the domestic market that had fueled their rise toward something larger. Here, amid the hum of conversations in different languages, the Greater Bay Area’s “two-hour supply circle” meets the world.

And, as Chan envisions, the next phase belongs to those who can lead through integration and internationalization — turning China’s scale into influence, its production into standards, and its technology into global recognition.

Next Actions

- Focus on core technology and brand strength, avoid price wars.

- Accelerate commercial vehicle electrification. Launch targeted subsidies and develop multiple energy solutions for electric buses, minibuses, and trucks to unlock the next growth segment.

- Support cross-sector collaboration between auto, AI, and energy grids to accelerate vehicle-grid interaction and intelligent cabin development.

- Treat Hong Kong not as a sales market alone, but as a strategic lab for adapting to international standards, and a go-global playbook development.

Contact the writer at stacyshi@chinadailyhk.com